By: Dr. Daniel Wolfe, J.D., PhD. Senior Director of Jury Consulting, Magna Legal Services

As part of an ongoing effort to examine COVID-19’s impact on prospective jurors’ attitudes and beliefs, Magna Legal Services conducted a series of nationwide surveys to assess evolving changes and shifts in perceptions in this brave new world.

Since the beginning of the pandemic in mid-March of this year, we collected responses from nearly 4,000 jury-eligible adults on a variety of topics, including:

• jurors’ propensity to show up for jury duty;

• the social and financial impact on individuals and corporations;

• perceptions of industry specific corporations; &

• the impact on jurors’ verdict and damages propensities in civil cases.

A particular area of interest, which has become a burgeoning hotbed of nationwide litigation efforts, is commercial insurance coverage litigation related to business interruption insurance claims. It is not uncommon for us to hear from clients that it is almost next to impossible to get a fair trial based on a commonly held belief that “jurors hate insurance companies.”

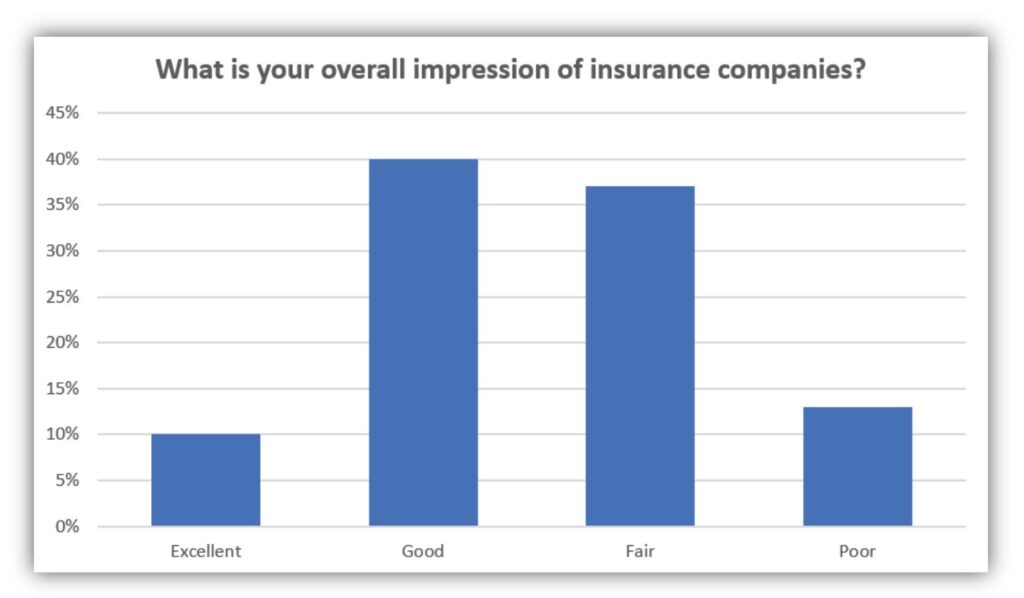

Our experience over the years demonstrates that most jury-eligible adults have neutral to positive experiences with insurance companies, most notably in the areas of health, auto, and homeowner insurance claims.

Notwithstanding the occasional parade of horribles with insurance claims that some prospective jurors lament, rarely do we see the level of insurrection from jurors that overrides their sense of fairness and justice in any particular case. That being said, we have seen demonstrable shifts in prospective jurors’ willingness to show compassion as a result of the pandemic.

Juror Perception of Insurance Companies: Post-COVID

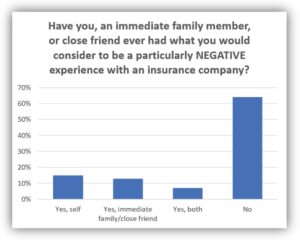

In our recent nationwide survey of 500 jury-eligible adults, we inquired as to prospective jurors’ experiences and general views of insurance companies. Less than one-quarter of the respondents reported that they personally, and/or their immediate family members or close friends, had a particularly negative experience with an insurance company.

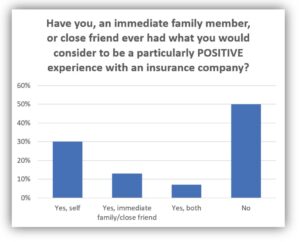

Alternatively, nearly 40% of the respondents reported that they personally, and/or immediate family members or close friends, had a particularly positive experience with an insurance company.

Perception on Business Insurance Claims due to COVID

More specifically, we asked our respondents to consider the following information regarding insurance coverage for business interruptions:

• Business owners may file claims requesting insurance money for the lost-income due to the interruption of business operations during the COVID-19 pandemic.

• Most business insurance policies contain language stating coverage is limited to business interruptions that are caused by direct physical loss or damage to the property.

With this information, nearly 70% of respondents agreed that any business interruption as a result of COVID-19 pandemic would be considered a direct physical loss or damage to property.

Surprisingly, nearly 80% of the respondents concluded that any business interruption losses that occur due to the COVID-19 pandemic should be covered by business insurance policies. These results suggest possible a Robinhood Effect: consumers simply want businesses, especially small businesses, to remain viable as a result of the devastating financial impact of the pandemic.

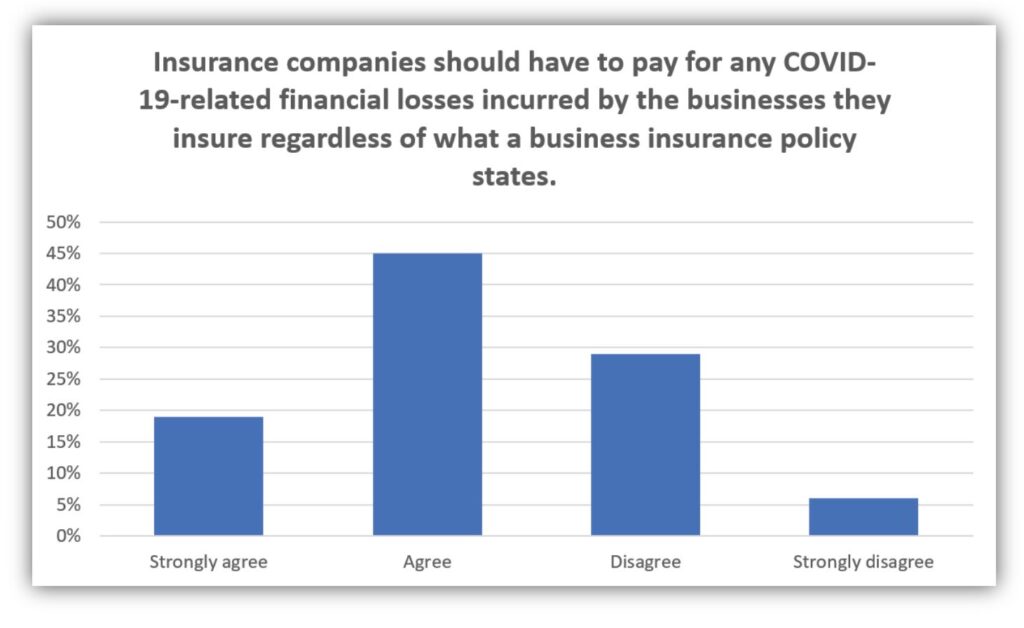

Nearly two-thirds of the respondents believe insurance companies should have to pay for any COVID-19-related financial losses incurred by businesses they insure regardless of what their policies state.

Arguably, jurors’ visceral responses to these issues may not necessarily be congruent with their decisions in an actual trial, where they have the benefit of both sides’ arguments and the full panoply of evidence.

Notwithstanding this ostensible limitation to the generalizability of these results, these findings demonstrate the willingness of prospective jurors to seek a resolution based on the perceived fairness and equity of the parties involved. This is also undergirded by the belief that insurance companies will have the financial wherewithal to weather the COVID-19 pandemic storm, and, therefore, would have the resources to “do the right thing” in paying for business interruption losses. Respectively, it is imperative to assess these personal experiences during voir dire given that some of these jurors’ reactions to these specific issues may be counter-intuitive.

Learn why Magna is named a “Best Of” winner every year by ALM for our Jury Consulting Services. Click below for a FREE case evaluation.